HOW BLOCKCHAIN CAN TRANSFORM THE MORTGAGE INDUSTRY

Most people, when they hear the term “blockchain” immediately think of Bitcoin and other cryptocurrencies. In fact, they may even think that blockchain and cryptocurrencies are the same, when in fact, they are two different things. Cryptocurrency, like the name suggests, is a form of digital currency whereas blockchain is a form of digital ledger. And while blockchain technology is used in conjunction with cryptocurrency, it can also be used for many other purposes including in the mortgage industry.

When used in the mortgage industry, blockchain can streamline the process and make everything more affordable.

WHAT IS BLOCKCHAIN TECHNOLOGY AND HOW DOES IT WORK?

In its simplest terms, blockchain technology is a method of conducting transactions digitally through multiple nodes or computers. The blockchain acts as a digital ledger which needs to be updated on each node each time there is a change to a transaction.

And because each node must be updated every time there is a change, the process is extremely secure and transparent.

Blockchain is a digital ledger or database that consists of 3 main parts:

The Record

This includes the details of individual transactions such as the personal information of the buyer, seller, and cost of the purchase. The transaction must be verified by the nodes in the chain before it becomes a part of the chain.

The Block

Records are then stored with numerous other records, which is called a block. Each block gets assigned its own unique code.

The Chain

Each block gets added to the chain.

The main difference between blockchain technology and other digital ledgers is the fact that the blockchain is decentralized. Instead of the information being stored on one central server, it is stored on a several different nodes, each of which must be updated when there is a new transaction.

Although it may sound like not having a central hub would be less secure, the opposite is in fact true. Because there are many different nodes, each one has to be updated every time there is a new transaction. This makes fraud extremely difficult if not impossible as every change can be tracked and is available to be viewed by anyone with access to the ledger.

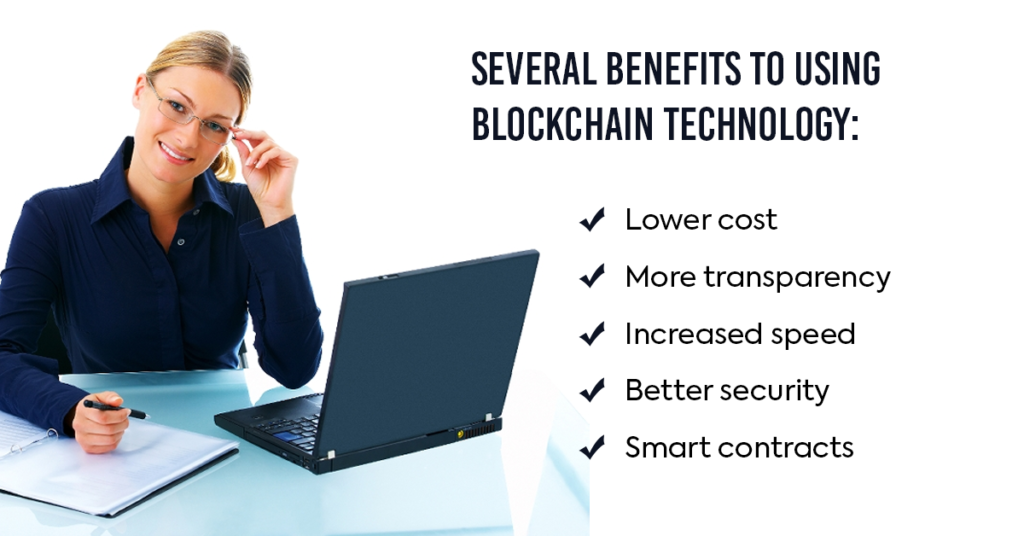

BENEFITS OF USING BLOCKCHAIN IN THE MORTGAGE INDUSTRY

From pre-qualification to application to settlement, the time it can take to finally obtain a mortgage can be anywhere from 30-60 days. With blockchain technology, a mortgage broker can easily track the process and it can move along much more quickly.

Blockchain is a digital ledger or database that consists of 3 main parts:

Lower Cost

In the mortgage industry, blockchain can help to reduce costs in a number of ways. During traditional mortgage transactions, a number of parties are involved and each one needs to get their cut. Blockchain can help eliminate the need for some of these third parties. Furthermore, blockchain can help reduce the risk of double transactions as well as eliminate the need to sift through piles of paperwork.

Increased Speed

if a change needs to be made to a transaction, the process can be completed in just a few seconds. This is much faster than traditional methods in which there must be multiple hard copies and back and forth between parties.

Smart Contracts

Smart contracts are contracts that can be triggered by an action taken by one of the parties. For example, if the person purchases home insurance, the mortgage can automatically be moved to the next step in the process.

More Transparency

with blockchain, it is impossible to make amendments to a contract or transaction without everyone else being alerted. This helps everything to be more transparent.

Better security

Because of the layers of verification and approval involved, blockchain is more secure than other forms of transactions.

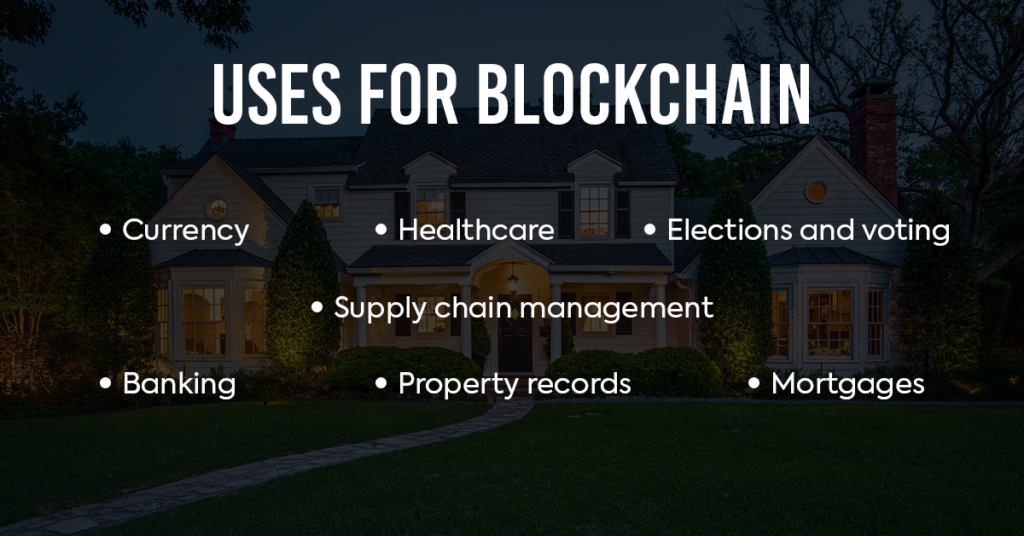

USES FOR BLOCKCHAIN

There are many uses for blockchain beyond what people currently think of. Some of its possible applications include the following:

Currency

Although Bitcoin is the most well known of the cryptocurrencies, there are several others. These currencies operate without the use of a central bank and instead use blockchain technology.

Healthcare

Privacy is a big concern in the healthcare industry. The security of blockchain makes it an ideal technology for the digital storing of patient records. Additionally, it streamlines the process for when data needs to be shared between a patient’s primary family doctor and other healthcare providers.

Elections and voting

Since blockchain is more secure than other technologies, it could be used to help prevent election fraud and vote tampering.

Supply chain management

Blockchain technology can be used to track parts and items within the supply chain and to verify their source.

Banking

Banks also use secure blockchain technology for keeping track of transactions as well as bill payments and loans.

Property records

Blockchain technology can also be used to verify property values, tax records, and past owners. This can come in handy when buying or selling a property to ensure all legal concerns are covered. Furthermore, it can help to reduce the cost of insuring a property.

Mortgages

Blockchain technology can help to streamline the mortgage industry in a number of ways. It can help to lower costs and make the industry more transparent. Overall, if used blockchain could reduce the potential for errors and make the process of getting a mortgage faster and more affordable.

BENEFITS OF USING BLOCKCHAIN IN THE MORTGAGE INDUSTRY

Although blockchain technology is extremely promising for the mortgage industry, it is of yet unregulated. There is no one standard yet when it comes to using the technology. Furthermore, if it is to be used, all parties have to be on board with it. One party cannot make a decision unilaterally that blockchain will be used. The final legal concern is that while blockchain is extremely secure, it is not impermeable – hackers may still be able to get into the system.

Contact Approved By James Team Today

Although blockchain technology isn’t yet standard in the mortgage industry, the experts at Approved By James Team are always at the forefront of the industry and are ready to embrace new technologies as it makes sense to do so. If you are looking for a qualified mortgage broker, contact us today for a consultation.

Blog Benefits of using a mortgage broker September 26, 2022 Approved by James Admin Entering the housing market can be as intimidating as it is exciting. While the thought of

Blog Should you refinance your mortgage? Time to find out October 3, 2022 Approved by James Admin Should you refinance your home as we approach the end of the year?

Blog Reviewing your credit score: Here’s how to do it August 29, 2022 Approved By James Admin Is it time to analyze your credit score? Reviewing your credit score isn’t